Chemistry Class for the BedroomWhen couples talk about having "chemistry" together, who knew it was such an accurate description?

The brain sends signals to NANC cells in the artery. The NANC cells release nitric oxide (NO). Nitric oxide acts as a signaling molecule and stimulates an enzyme called guanylate cyclase in nearby cells. The guanylate cyclase converts a chemical called GTP into another chemical called cGMP. cGMP causes muscles in the walls of the arteries to relax. This relaxation increases blood flow. Meanwhile, PDE is decomposing the cGMP and turning it back into GTP. There is a cycle -- guanylate cyclase turns GTP into cGMP, and PDE turns cGMP into GTP. Nitric oxide turns the cycle on. cGMP is produced as long as the brain is sending messages down the nerve fibers in the artery, which generate nitric oxide and keep the cycle going. When the brain stops sending the signal, all of the cGMP goes away because PDE is deactivating it. This way, the brain can turn valves on and off whenever it wants to. So how does this relate to an erection? When the brain gets aroused, it sends a signal to the penis. Nerve cells in the penis' corpora cavernosa start producing nitric oxide, which leads to the creation of cGMP. The cGMP causes arteries in the corpora cavernosa to dilate, causing lots of blood to flow into the penis. The extra blood flowing in causes the penis to inflate like a balloon. An erection occurs. When a man has erectile dysfunction, there can be many reasons for the problem. But one of the most common reasons, especially in older men, is that the arteries in the penis aren't dilating enough when the brain sends the signal. The man is aroused and the nerves in the penis are producing nitric oxide, but the amount of cGMP produced isn't enough to maintain an erection. The way that Viagra goes about solving this problem is quite ingenious. Ads by Google"Why Pills Can't Fix ED?"How I Stopped Taking ED Pills And Fixed My ED With 1 Strange Exercisemalehealthcures.com/ImpotenceCauses5) Foods To Never EatHere are 5 foods you should never eat if You want to lose belly fat.perfectorigins.com/5BadFoods.phpSocial Mktg CampaignsPlan Your Day to Day Social Mktg. Download Free Proven Tactical Plan!marketo.com

0 Comments

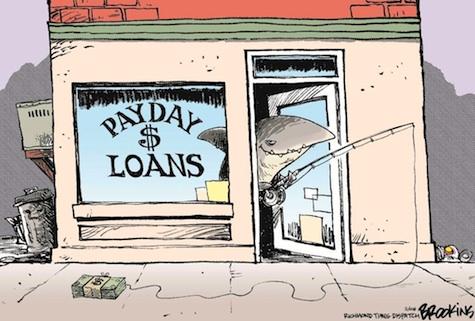

As consumers move their financial activities online, applying online for a payday loan may seem like the natural thing for a cash-strapped person to do.

But you could be setting yourself up for a world of hurt, from paying exorbitant interest rates to having funds swiped from your bank account to being threatened by debt collectors. Just filling out an application could be enough to begin the harassment and thievery. "Absolutely the worst thing you can do is apply for an online payday loan," says Jay Speer, executive director of the Virginia Poverty Law Center. Most online payday loan sites aren't even operated by lenders. They're run by "lead generators," who seek your personal information, such as Social Security number, driver's license number and bank account details. They then sell that information to lenders. "Your email and telephone explode after that," Speer says, as lenders vie to offer you cash. That can happen even if you live in one of the 15 states where payday loans are illegal. Lenders aren't the only ones in the market for your personal information. "There's a good chance they sell to fraudsters -- people who come after you months or years later," he says. Sandra Green (not her real name) has experienced this firsthand. The Virginia woman turned to online payday loans after her husband was injured and couldn't work for two years. Their credit was damaged and they couldn't get cash to pay their bills from traditional financial institutions. Green took out several loans totaling $3,000 to $4,000 starting around 2010. The lenders that she received cash from took their payments from her bank account -- but they weren't the only ones. A company she had never heard of swiped money from her account, creating an overdraft. She filled out a request for the bank to stop payment. That worked for about six months, and then the withdrawals started again. "People will change the identity of the company and then they'll hit it (the account) again. Once they do this it's a never-ending cycle," she says. Companies she'd never done business with would call her at work and at home, harassing her. One threatened to file papers with the local sheriff's office if she didn't pay immediately. "They get really belligerent when you don't do what they want you to do," Green recalls. She feared she'd wind up in bankruptcy because of the loans and finally sought help from Blue Ridge Legal Services, a Virginia legal aid society, in 2013. Blue Ridge connected her with the Virginia Poverty Law Center. Speer says of online payday lenders: "These people are like sharks. If you give them some money it's like throwing blood in the water." These people are like sharks. If you give them some money it's like throwing blood in the water. -- Online payday loan customerPayday loans are generally described as small, short-term loans. A consumer writes a check for the amount borrowed, plus a fee. The lender advances money against the check and the check is held until the next payday, when the loan and fees must be paid. Or, in the practice used by most online lenders, a consumer can grant the lender access to his bank account, and the lender electronically accesses the account to deposit money and withdraw payment. Even paying back legitimate loans carries astronomical costs. Green took out a loan of $350. It took six weeks for her to pay it back, and she paid nearly $300 in fees. Online payday loans boom Her experiences are not uncommon. "Fraud and Abuse Online: Harmful Practices in Internet Payday Lending," a 2014 study by the Pew Charitable Trusts, found online installment payday loans typically have an APR of 300 percent to more than 700 percent. Online lump-sum payday loans have a typical APR of 650 percent, or $25 per $100 borrowed per pay period. Exorbitant fees are also charged, and initial payments might not be applied to the loan's principal. Online payday lending is big business. Revenue tripled from $1.4 billion in 2006 to $4.1 billion, according to Pew. Of the more than 250 online payday borrowers surveyed by Pew, almost 40 percent said their personal information was sold to a third party without their knowledge. Nearly one-third had an unauthorized withdrawal from their account. Threats were common, with 30 percent of those surveyed saying they were threatened by an online lender or debt collector. "Harassment and fraud are really concentrated in the online lending market," says Nick Bourke, project director for Pew's study on payday loans. Part of the problem stems from the fact that there's no control over who can get your information once you apply for an online payday loan. "People's personal information can be spread far and wide," Bourke says. Even if the loans are fraudulent, a consumer's failure to pay them may be reported to one of the three main credit bureaus, Speer says, which can impact a consumer's ability to rent an apartment or land a job. Many storefront payday lenders are fed up with the behavior of these online payday lenders. "These unlawful lenders roam the Internet trolling for customers. They are scammers. They are fraudsters," says Amy Cantu, spokeswoman for the Community Financial Services Association of America, which represents more than half of the country's storefront payday lenders. Though online payday lenders represent just one-third of the marketplace, 90 percent of payday lending complaints filed with the Better Business Bureau are aimed at them, according to Pew. Self-regulation efforts Association members vow to adhere to the organization's best practices, which include complying with state and federal laws, being licensed in each state in which they do business and adhering to acceptable debt collection practices. Some of the association's larger members also have an online presence, she says, but those sites also adhere to the organization's best practices. Cantu says she understands that consumers with financial troubles may prefer the anonymity of the Internet when seeking cash, rather than walking into a storefront payday lender. But online lenders are supposed to only operate in the states that allow payday lending.Her organization wants the federal consumer watchdog agency, the Consumer Financial Protection Bureau, to crack down on illegal lenders. Agencies crack down Already the CFPB and the Federal Trade Commission are stepping up action against fraudsters. In a joint news conference in September, the agencies announced they'd filed suit against two online payday lenders. These unlawful lenders roam the Internet trolling for customers. They are scammers. They are fraudsters -- Amy Cantu, Community Financial Services Association of AmericaThe CFPB sued Kansas City-based Hydra Group, while the FTC sued CWB Services, also based in Kansas City. The CFPB received more than 1,300 consumer complaints about the Hydra Group. At the news conference, CFBP Director Richard Cordray accused the Hydra Group of "running an illegal cash-grab scam to force purported loans on people without their prior consent. It is an incredibly brazen and deceptive scheme." Both the Hydra Group and CWB Services were accused of buying personal information, including bank account numbers, from lead generators. The companies would deposit money into consumers' bank accounts without any signed agreements, and then make unauthorized withdrawals from the accounts. If a consumer complained, the companies would produce false loan documents. In 15 months, the Hydra Group made $97.3 million in loans and collected $115.4 million from consumers. Even if consumers closed their accounts, their information might have been sold to debt collectors, who then attempted to collect more money. A federal judge temporarily shut down the Hydra Group, freezing its assets. The CFPB is requesting a permanent shutdown, along with penalties imposed upon the company and refunds made to consumers. With CWB Services, the federal court froze the company's assets and appointed a receivership and the FTC is requesting consumers' money be refunded. The company had raked in $46 million in 11 months, said Jessica Rich, the FTC's director of the Bureau of Consumer Protection. Bourke says the CFPB should ensure that small loans are tailored to the borrower's ability to pay them off and should provide more protection to consumers, particularly against illegal debt collection practices. "The core of the problem is that payday loans don't help people. They drive people further into debt and distress," he says.  It seems like payday loan offers are everywhere these days. From the local strip mall to the Internet, the payday lending industry is booming. But what is a payday loan? Is it as bad as some people say? Credit.com gives you straight answers about payday loans:

What is a Payday Loan?Payday loans can be very costly. Borrowers should use them with caution and pay the amount back as soon as possible. These loans are usually priced at a fixed dollar fee, which represents the finance charge to the borrower. Because the loans have such short terms, the cost of borrowing is very high. In return for the loan the borrower usually provides the lender with a pre-dated check or debit authorization. How Does it Work?Say your car broke down and you decide to borrow $300 for the repairs from a payday lender. You’ll write a post-dated personal check for $340 (the amount plus a finance fee) made payable to the lender. You enter this information online when applying for a payday loan through the internet. The lender then advances you $300 for a set period, usually 14 days. When that period is up, you pay the lender $340 in cash, let them deposit the post-dated check or write another post-dated check for the amount plus an additional finance fee. If you do not pay the debt in full at the end of the term, you will be charged additional fees and finance charges. Get a Free Credit.com AccountSign up for Credit.com and get your FREE Credit Score & Personalized Action Plan to help improve it. Free & updated every 30 days. Get Started Now »Who Uses These Types of Loans?Generally, anyone with a checking account and steady income can obtain a payday loan. However, it is most common for borrowers who don’t have access to credit cards or savings accounts to use this type of lender. Since these loans don’t require a credit check, people with no credit or credit problems often turn to payday loans. Military personnel and recent immigrants also commonly use payday loans. What Are the Benefits?Payday loans can be a good tool for quickly and easily borrowing cash during an emergency if you don’t have other financial options. For example, you might use a payday lender for an immediate and temporary financial need such as a medical bill, car repair or other one-time expense. Payday loans are helpful for people who don’t have credit cards or savings available. Because the loans do not require a credit check, they are easy for people with financial problems to obtain. What Are the Negatives?It is crucial that you repay a payday loan as soon as possible. Many people get into trouble with these types of loans when they are unable to quickly repay the debt. If you can’t repay the loan at the end of the term, you’ll be charged expensive additional fees. It is very costly to be stuck in a payday loan cycle for a long time and can lead to larger financial problems. Payday loans are also much more expensive than other methods of borrowing money. In most cases the annual percentage rate (APR) on a payday loan averages about 400%, but the APR is often as high as 5,000%. A standard credit card has an APR of 12% and a standard loan APR is around 7%. If possible, it is better to use a credit card or tap into your savings in the event of an emergency. What About Usury Laws?Numerous states have very specific laws that regulate the lending industry. Called “usury laws” these regulations define permissible lending terms and rates. Some states also have laws that regulate the amount a payday lender can lend to consumers and how much they can charge for the loan. Other states ban payday lending outright, such as New York. These laws vary widely. Payday lenders often work around these regulations by partnering with banks based in other states, such as Delaware. It is important to read the fine print on the payday loan offer and understand your consumer rights. You can read Credit.com’s summary of state-by-state payday loan restrictions online. Should I Apply for a Payday Loan?Before you consider applying for a payday loan, step back and consider your options. Ask yourself if it really is an emergency. Payday loans can be helpful for one-time emergency costs such as medical fees but are not a good idea for funding unnecessary expenses. Is it possible to wait to repair your car or pay your bills until your next paycheck? Remember, a $25late fee on a bill is cheaper than a $40+ finance charge for a payday loan. Think about other ways to borrow money: Alternatives to Payday Loans

When consumers with poor credit and little savings need cash in a hurry, payday loans can seem like the best choice out of limited options.But payday loans come with a slew of risks and disadvantages, the most egregious being sky-high interest rates and lack of transparency about fees.

Thirteen states have even banned the practice outright or passed prohibitive usury laws. Whether you use payday loans on a regular basis or only once in a while, you should be aware of the industry’s most troubling statistics, then consider your other options: While APR on a bank-issued personal loan generally ranges from 10%-25%, the APR on a payday loan ranges from 300% to over 700%.

Small-dollar loans from financial institutions The growing demand for small-dollar loans has enticed some banks to start offering loans of less than $1,000 for the first time. In fact, the FDIC initiated the Small-Dollar Loan Pilot Program in 2008 expressly to increase the availability of fair, affordable alternatives to overdraft protection fees and pricier loans offered by payday lenders. Their APRs range from 5% to 36%, so shopping around for the best rate is still a good idea. Credit unions have also jumped on the small loan bandwagon. In 2010, the National Credit Union Association (NCUA) instituted the Short Term Small (STS) Loan Program, permitting federal credit unions to offer STS loans of between $200-$1,000 with APR of 28% or less. Successful repayment of an STS loan can improve the borrower’s credit and help them access loans with lower interest rates in the future. Cash advance from employer Asking your supervisor for an advance on your next paycheck can be awkward, but don’t let that deter you if you’re really in a bind. As long as you’re in good standing with your company and don’t make a habit of it – asking more than once is almost certainly a bad idea – this is a safe solution to a financial emergency. You’ll be avoiding exorbitant interest rates and, since this type of request is a one-time deal, there’s no opportunity for the advance to snowball into a larger amount of debt. Some HR departments even offer preprinted forms for requesting payment advances. You’re the best judge of whether this request could be frowned upon by your employer, but meeting with your boss to calmly explain why you need an advance just this once will likely be met with an understanding response.Secured credit card Applying for a secured credit card can be an excellent option for individuals with poor or no credit. This type of credit card requires the user to provide a cash deposit (usually between $300 and $500), which serves as collateral and determines the credit line. Once the deposit is paid, a secured card can be used just like any other for emergency purchases, monthly bills and everyday expenditures. There are as many predatory options out there as there are safe, reliable ones, so be sure to shop around for a card that comes with a low interest rate and minimal annual fee. Secured credit cards also provide another benefit – they’re a great first step toward rebuilding poor credit. Military aid societies and other affinity groups If you or someone in your family has served in the military, special financial aid may be available to you. Military aid societies like Army Emergency Relief (AER), Air Force Aid Society (AFAS), Coast Guard Mutual Assistance (CGMA) and Navy Marine Corps Relief Society (NMCRS) offer grants and interest-free loans to military personnel and their immediate families. These programs are designed to assist with essential expenses, such as groceries, rent and medical bills. Be sure to check out state-specific programs as well, like the California Military Family Relief Fund and California National Guard Financial Assistance Fund. SimpleFi, an affiliate-based lender, also provides low-interest, short-term loans to active duty military, teachers, and first responders (police, fire fighters, and EMTs). What if I’m already trapped in the payday loan cycle? If you’re struggling to pay back an outstanding amount to a payday lender, avoid rolling over your balance into yet another loan at all costs. Next, get in touch with a credit counselor who can best advise which of the above options are best for you and can help you create a plan for managing your debt. Be cautious when choosing a credit counselor; find out through your local Attorney General and consumer protection agency whether users have ever filed complaints against the counseling service and avoid agencies that require significant payment up front. Above all, make payday loans your last resort – their convenience simply doesn’t outweigh their hefty risks.  Rafael Palmeiro seems an unlikely Viagra pitchman. The Texas Rangers slugger is only 37 and won't admit to having erection problems, yet he recently agreed to appear in ads promoting the drug. The deal has made people wonder whether Palmeiro really represents men with erectile dysfunction, or whether Pfizer, the company that makes Viagra, wants to persuade young men to try it for fun.

It's true that erectile dysfunction is more common in older men, but many potential Viagra users are hardly senior citizens: About 40% of 40-year-old men in the U.S. have some degree of erectile dysfunction. Most Viagra users today, according to Pfizer, are in their early to mid 50s. So it makes sense that the company would want to reach more men around Palmeiro's age. Urologist Myron Murdock, medical director of the Impotence Institute of America, says these men are likely to use Viagra because sexual performance is a high priority for them. A younger man, Murdock says, "wants his V-12 Jaguar working just perfectly," whereas an elderly gent may be content with less dependable erections. What's more, the sexual partners of younger men "are more demanding of their performance," Murdock says. Pfizer denies that it's promoting Viagra for recreational use. "We've consistently opposed that," says spokesman Geoff Cook. Nevertheless, Murdock says it's fine to pop the little blue pill to "optimize" your sexual performance. We assume all young men have normal sexual functioning, "but they're really not normal," Murdock says. Hardening of the arteries, which restricts blood flow to the penis, can begin during the teen years, so that by the time a man is in his 20s, his ability to get and keep an erection has already begun to decline. Murdock says many men who seek Viagra for recreational use actually have minor erectile dysfunction. There's also some evidence that Viagra can shorten the time it takes a man to recover after sex and be ready for another round. This is called the "refractory period." Normally it lasts 20 minutes or longer. One study, published in the journal Human Reproduction in January 2000, found that Viagra shortened the refractory period by about 10 minutes in healthy men.  Q: I am a 27-year-old and sometimes take to please my girlfriend. Is it harmful for my health? What about my future sex life? Will I always have to take them?

All the different tablets mentioned here have the same chemical composition – Manforce and Pengra are actually the desi versions of Viagra, which in turn is the brand name of the generic drug sildenafil. In countries like the US or UK, the drug is only available through prescription but lax laws in India means that it can be easily purchased over-the-counter. One thing you’ve to clearly understand is that Viagra is a drug to beat erectile dysfunction and it’s not an aphrodisiac or libido booster. In simple words, it will only give you an erect penis when you’re aroused. Now the drug is most commonly used by people in their 50s and 60s, those at an age where there heart finds it hard to pump enough blood to the penis to maintain an erection. However, recent studies have shown that the recreational use of Viagra has gone up among youngsters. Most doctors recommend that the drug shouldn’t be used like this because one’s body can get dependent on it and you could reach a phase where you will find it hard to get hard without the drug. There are other harmful effects as well. You shouldn’t take the drug if you are taking other medicines which contain nitrates. These are usually used to treat chest pain,hypertension and other such ailments. Some of the other common side-effects are facial flushing, headaches, liver problems, heart attacks (rarely), blurred vision, bluish vision and sensitivity to light. The most infamous side-effect though is erections which last for four or more hours. Sometimes these erections can be extremely painful as well. If you experience that you should call a physician and visit a hospital immediately. In conclusion you should definitely stop using these drugs; they are not for recreational use or to show off your sexual prowess but an aid for men really suffering from a problem. Read more about kegel exercises that can help you beat erectile dysfunction. Click on the picture below to view photos on – 8 things you didn’t know about Viagra. Image source: Getty Images For more articles on male sex problems, check out our male sex problems section.  Viagra is now being used to treat not only erectile dysfunction (ED) but also pulmonary hypertension. And the drug may have potential for treating several other conditions, according to a recent report. The three ED medications currently on the market—Viagra, Levitra, and Cialis—all work by the same means, and they have similar side effects.

The most common are headaches and facial flushing, which occur in 15% of men. Other reactions include nasal congestion, indigestion, and back pain. These side effects are mild and temporary. The most important worry about ED pills is their ability to widen arteries enough to lower blood pressure. And men who are taking nitrates should never use any of the ED pills. Although some of the drugs’ side effects may be troublesome, others may be helpful, and scientists are studying whether ED pills might help treat a variety of nonsexual problems. Viagra (sildenafil) has been on the market longest and is most studied. It’s yet not clear if the other ED pills offer similar benefits, but Viagra, at least, may prove useful for some other conditions, including these: Pulmonary hypertension Viagra is now marketed under the name Revatio for this uncommon but serious disorder of high pressure in the blood vessels leading to the lungs. Mountain sickness Viagra can reduce pulmonary artery pressure at high altitude and improve the ability to exercise in low oxygen conditions. Raynaud’s phenomenon In affected individuals, exposure to the cold triggers spasm of the small arteries that supply blood to the fingers, toes, or both, which become pale, cold, and painful. Both Viagra and Levitra have been helpful in clinical trials. Heart disease Studies suggest Viagra might help patients with congestive heart failure or diastolic dysfunction. Further details are published in the August 2007 issue of Harvard Men’s Health Watch. Story Source: The above story is based on materials provided by Harvard Medical School. Note: Materials may be edited for content and length. The phone rings and a scary voice on the other end tells you that you owe them money and need to pay up … or else. The caller leads you to believe that a recent loan you took out has come due and that its time to pay or face legal action. Frightening, right?

This terrifying scenario has been experienced by thousands of consumers in recent years due to con artists running the “phantom debt collector” scam. In recent weeks, consumers have contacted Fraud.org in increasing numbers, suggesting the scam is once again on the rise. The phantom debt collection scam comes in a number of variations, but the common element in almost all of them is a claim that a consumer owes money on a debt and needs to pay or else face serious consequences. Often, the scam begins when a consumer inquires about a payday loan or other short-term credit online or over the phone. The Web site or phone number that the consumer contacts may or may not be associated with a legitimate lender. Regardless of whether the consumer actually takes out a loan, he or she may receive a call later demanding money be paid. Since consumers interested in payday loans are often financially strapped, they may be susceptible to such demands whether or not they actually took out a loan. Even for consumers who do not have outstanding debts, the con artists are threatening and convincing and have led some consumers to wonder whether someone has taken out loans in their name. In cases where a consumer actually does have outstanding loans, the scam artist may claim that the victim owes far more in fees and interest than he or she actually does. In other cases, the victim of the scam may be behind on a loan, but the caller has no authority to actually collect on the debt. No matter the consumer's actual situation, skilled con artists are convincing them to hand over precious cash to settle the "debt." Scammers often demand payment on these phantom debts via wire transfer, credit or debit card. In a major enforcement action brought by the Federal Trade Commission in 2012, scammers working out of call centers in India claimed to be law enforcement officers who threatened to arrest victims if money was not paid. One outfit alone made at least 2.5 million calls, collecting more than $5 million before it was shut down. In other recent cases, the scam artists, again apparently working out of India, have threatened a negative credit report if payment is not made. Consumers should be on the lookout for these scams. Here are some tips for spotting and avoiding being a victim:

You need money—$300 to be exact. You feel like you have no alternative, and the cash on those billboards is inviting.

So you visit a payday loan outlet. Mouse over the image to find out the annual interest rate for that $300 payday loan." How Much are you Paying for that Loan? If you want to borrow $300 from a payday lender, you pay a fee, usually $20 per $100 that you borrow. So you write a check to the payday lender for $360. At the end of the two weeks, if you're like most people, you have to roll the loan over and pay another $60. The $120 you pay to borrow $300 for one month translates into a 520% annual percentage rate (APR). The annual percentage rate is calculated on the cost of rolling the loan over every two weeks, for a year. You calculate it by multiplying the two-week interest charge ($60) by 26 two-week periods per year ($60 x 26 = $1,560). You'd pay $1,560 to use $300 for one year. To figure out the annual percentage rate, divide the amount you'd pay for the loan in a year, by the loan amount: $1,560 /300 = 5.2. Multiply by 100 to get 520%. Some sources say they've seen payday loans with APRs as high as 7,000%! CloseYou write a check for $360. The lender gives you $300 in cash, and keeps $60 for her fee. She says she'll cash the check you wrote in two weeks, unless you return to roll over the loan. True story This is a true story. A member of Florida Central Credit Union (FCCU) used a payday loan outlet to borrow $300. By the time she turned to her credit union for help, the woman had paid $1,100 in fees on the $300 loan. And she still owed the original $300! She also owed money to six different payday lenders, says FCCU CEO and President, Ed Gallagly. "This is very common. Herein lies the real problem with payday loans," explains Gallagly. The real problem Most people can't pay the loan back in two weeks. Many people find themselves short of cash—especially when they just start out on their own. "Payday-to-payday is how most of us live," says Jim Blaine, president and CEO of State Employees Credit Union. Payday loan commercials tell you it's quick and easy to borrow: you write a post-dated check and they give you cash on the spot. They hold the check, and don't cash it until your next payday. The commercials don't mention that you're paying outrageous amounts for the loan. Payday lenders know that if you didn't have enough money this payday, you probably won't be able to pay your other bills, plus the loan, next payday. They count on you to roll the loan over. And over. And over. That small fee quickly adds up to a sum larger than the original loan. "If you talk to the trade association for the payday lenders, they say rollovers are infrequent, but that's not true and they know it," says Blaine. What about me? Keep your credit report clean. Roughly 10% of all payday loans are made to people ages 18-25. The cell phone bill is due and they don't have the money. And it's a big one. That's why it's so important to start saving now. "You can count on needing money when you least expect it. Start saving for emergencies at an early age," says Vicki Jacobson, president of the Foundation for Credit Education in St. Louis, Mo. The trap Is a pawnshop loan a better deal? You haven't put aside any money for emergencies, and you lose your job. Bills still come in. Payday lenders lure you with their friendly service and ease of use. They don't run a credit check, and you walk out the door with cash in your hand. Many payday lenders even stay open 24 hours a day. What could be easier? "You go into one of these places to cash checks or to get a payday loan, and they treat you like a friend," says Gallagly. "Their software for check cashing and payday loans is very sophisticated. They build up a database on you." "They know you; they know your family, Gallagly adds. They know if you're married; they know if you have children; they know your birth date." The convenience comes at a price—your loan's completely to the payday lender's advantage. Another solution If you are tempted by a payday loan, check your credit union first. If you are tempted by a payday loan, check your credit union first. Some credit unions offer a lower-cost small loan with an APR between 15% and 18%. Compare that to a payday lenders' rate of 500% or more. At Florida Central Credit Union, "we're realistic enough that we don't make the loan for two weeks," Gallagly says. "We ask, 'how much do you feel you could comfortably pay a week?'" Gallagly says Florida Central gives lenders a payment period "more like three months, six months, nine months, or twelve months." Other credit unions, like State Employees Credit Union, offer members another kind of alternative to payday loans. Members can borrow up to $500 at 11.75% APR—which amounts to about $2.50—for two weeks. Compare this to a payday loan of $500 at 520% APR—which amounts to $100—for two weeks. Do your research Borrowing money is a business relationship, Blaine explains. A lot of young adults don't realize that they can negotiate the terms of a loan. "If you don't know that borrowing money is negotiable, don't know how to bargain, and don't know what the best price is, then you're always at a disadvantage," says Blaine. Compare borrowers who use different lenders. Start your research at your credit union. Then, check the borrowing costs at a bank and payday lender. "A payday loan is a last resort. Let's face it, even a cash advance on a credit card is typically cheaper than a payday loan," says Jacobson. But, before you decide you need a loan, ask yourself, "why?" Gallagly says many people who use payday lenders don't have an emergency. Stop the bleeding While debts to payday lenders can cause you emotional and financial stress, they're not the end of the world. Help is available. "I hate to encourage people to borrow to get out of debt, but this is a case where the bleeding has to be stopped. This is a high-priority debt," Jacobson says. Use a budget to know exactly how much you can spend. First step in ending a payday loan debt is to stop the interest from accumulating. One way to do this is to borrow from a credit union to pay off the loan and set up a payment plan at a lower interest rate. If that's not possible, a local Consumer Credit Counseling service can help. "Counseling is free (some may charge a small set-up fee for debt management program)," Jacobson says. "Reputable nonprofit counseling agencies act on behalf of the consumer to negotiate with credit issuers to reduce monthly payments." The next part of the cure is to set up a budget. A detailed budget helps you develop your financial goals and know exactly how much you can spend without getting into trouble. The National Foundation for Credit Counselling has a network of member agencies that provide help with budgeting or debt management. Something to think about "This past year's college graduate is facing about $3,000 in credit card debt and $17,000 in student loans," Jacobson says. "Now, if they don't get that prized job..." You can see where she's going with that. Today's job market is tighter than just a few years ago. Many people today graduate college and have trouble securing employment in their fields. Jacobson says our culture is "expecting a lot out of young people to pay that all back at a very early age." She asks, "If we're expecting all of that out of people in their early 20s, is it any wonder that 10-15 years later, they're getting payday loans and debt management programs?" Jacobson's advice: "Think twice about pledging your future, unearned income to pay off what your borrow today." |

RSS Feed

RSS Feed